NVR - Demand through Financial Discipline

In 1992, NVR Inc. filed for Chapter 11 bankruptcy. The company had done what most American homebuilders do in a rising market: it bought land. Raw land, in volume, on the balance sheet, at the peak of a cycle. When the market turned, the land didn't move, and the debt didn't shrink.

What emerged from the restructuring was not just a leaner balance sheet. It was a fundamentally different theory of how a homebuilder should relate to demand. NVR would never again speculate in land. It would offer an option—paying a modest fee for the right to purchase finished lots at a fixed price, exercising that right only when a homebuyer had already signed a contract. No buyer, no lot purchase. No lot purchase, no land on the balance sheet. No balance sheet land, no sunk-cost pressure to sell whatever configuration the market seemed to want.

The bankruptcy produced the balance sheet. The balance sheet produced the discipline. The discipline produced the factory. And the factory produced one of the most durable financial performances in American homebuilding.

The Intervention: The Land Option as Structural Moat

The American volume homebuilding industry has a structural problem that appears to be a feature. Buyers want choice; developers offer choice. This choice fragments the product specification, which prevents standardized procurement. Since no factory investment is justified, no learning curve develops, and costs remain unpredictable. A builder carrying land on its balance sheet has one overriding imperative: move the inventory. The home specification follows the land; it does not lead it.

By utilizing land options rather than speculative land ownership, NVR ensures that confirmed buyer demand precedes every capital commitment. This rigid sequence, in which a homebuyer signs a contract before NVR exercises its option to purchase a finished lot, turns the buying decision into a functional "call" on the entire supply chain.

NVR Manufacturing Line. Source: NVR

Then, NVR integrates around the transaction. By controlling the customer relationship, the sales funnel, and the product menu through its Ryan Homes, NVHomes, and Heartland Homes brands, NVR eliminates uncertainty for its vertically integrated factory infrastructure. Buyer demand triggers the lot purchase, which in turn triggers the build, while mortgage and title services are integrated to capture more of the transaction and reduce friction for the buyer. NVR uses regional density to create coordination advantages.

NVR has systematically reinvested its balance sheet strength to expand its regional manufacturing footprint, building factory capacity in strategically selected metros where developer networks are mature and volume can justify fixed capital investment. This deliberate geographic sequencing has allowed NVR to scale its manufacturing infrastructure and build a competitive moat without the speculative risk that triggered the 1992 bankruptcy.

While NVR relies on subcontractors for on-site construction, it creates an industrialized business system by converting uncertain market demand into a staged sequence of commitments.

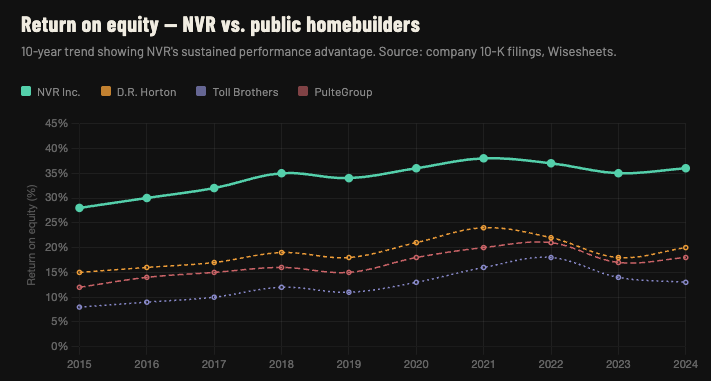

This sequence is the core strategy: the result is neither a fully industrialized process nor a completely vertically integrated system. It is an industrialized business system operating inside the constraints of American homebuilding, and it is working. In fiscal year 2024, NVR reported record revenue of $10.6 billion. NVR’s return on equity consistently exceeds 30 percent, representing the highest sustained profitability in public homebuilding.

The moat is the system; the system begins with the balance sheet.

The Model

NVR’s land option model is both a risk-management strategy and a strategic demand unlocker.

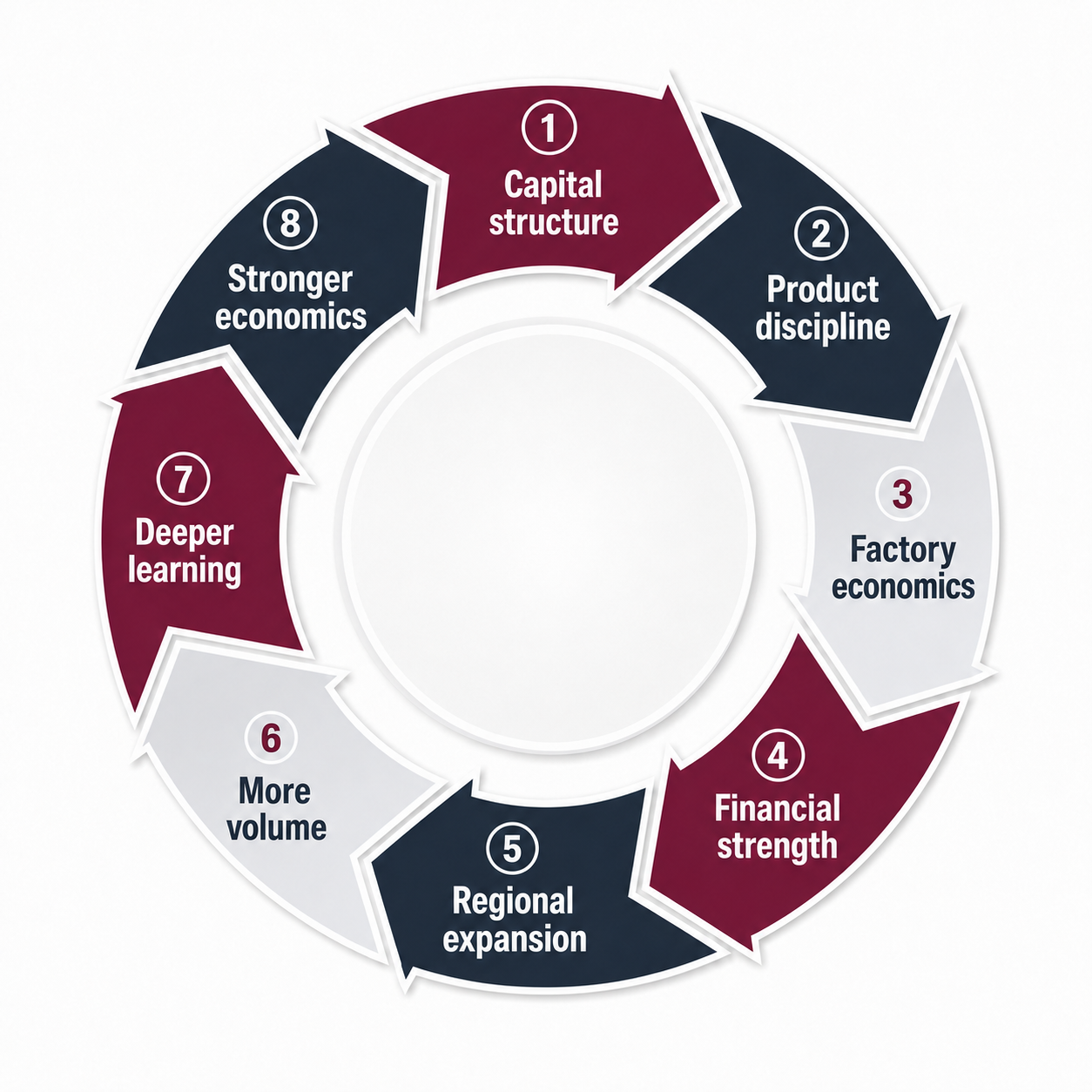

By making the land option the trigger for the entire homebuilding process, NVR converts its balance sheet structure into an operating discipline. The sequence is mandatory: confirmed buyer demand precedes every capital commitment. No buyer, no lot purchase. No lot purchase, no build. No exceptions.

The land option creates discipline as the path of least resistance and customization as the path of most resistance.

The capital structure enforces product standardization

Because NVR carries no speculative land inventory, it has no sunk-cost pressure to vary the product. The buyer selects from a controlled menu of standardized floor plans. The product does not chase the market—the product is the market offering.

Standardization enables factory economics

With predictable product specifications, NVR can commit to long-term supplier relationships, volume purchasing agreements, and regional manufacturing partnerships. The learning curve runs because the product does not change from project to project.

Factory economics generate balance sheet strength

NVR's return on equity consistently exceeds 30 percent—the highest sustained profitability in the public homebuilding sector. This financial performance creates capital for strategic reinvestment.

Balance sheet strength enables regional expansion

NVR systematically reinvests to expand its manufacturing footprint, building factory capacity in strategically selected metros where lot developer networks are mature, and volume justifies fixed capital investment. This deliberate geographic sequencing—entering a market only after confirming sustainable demand density—compounds the advantage.

The flywheel is now the strategy. Each successful cycle deepens the competitive moat, proving that industrialization is not just about how you build, but how you structure the right to build.

The standard is the standard because the land option creates the call.

The Limits

The model has distinct structural limits. First, it relies on geographic dependence: NVR's strategy works best in secondary and tertiary markets with active third-party lot developer networks. In high-density metros or areas with slow entitlement processes where finished lots are scarce, the model struggles to operate because the strategy is inseparable from the availability of finished land.

Second, there is a necessary trade-off in production acceleration. Because NVR does not own raw land, it cannot pull forward supply by accelerating development during a housing boom. While the land option model provides structural discipline in down cycles, it limits upside velocity in rising markets compared to builders who carry land on their balance sheets.

Finally, the industrialization of the business system remains incomplete. While lots are optioned, NVR has not yet extended this same logic to the supply side to secure factory capacity through multi-year confirmed commitments. Extending the option logic across the full value chain, from lot to module to on-site construction, represents a potential next step.

Where to Start

The NVR argument reduces to one primary question: what in your capital structure or contract architecture makes product discipline the path of least resistance?

This question means moving from speculative variety to structural commitment:

Multifamily Developer: Structure land acquisition as an option contingent on signed purchase agreements or pre-leases. This removes the inventory pressure to vary the specification to "chase" the market.

Public Housing Authority: Commit a multi-site program to a single standard unit type, structuring procurement such that subsequent site releases are contingent on the previous site’s delivery performance.

Corporate Real Estate: Negotiate master supply agreements against a defined product catalog, fixing specifications and price schedules over a multi-year term to incentivize supplier investment.

NVR’s lesson is not that every builder should avoid land. Industrialization requires a demand trigger that disciplines the rest of the system. The land option creates the call.

Create a structure in which confirmed demand pulls the system forward, product discipline is easier than customization, and thus every expansion and integration is justified by repeatable volume.